The Real Cost of Living

Empirical Proof that 2019 to 2024 Inflation Is Much Worse Than You Think

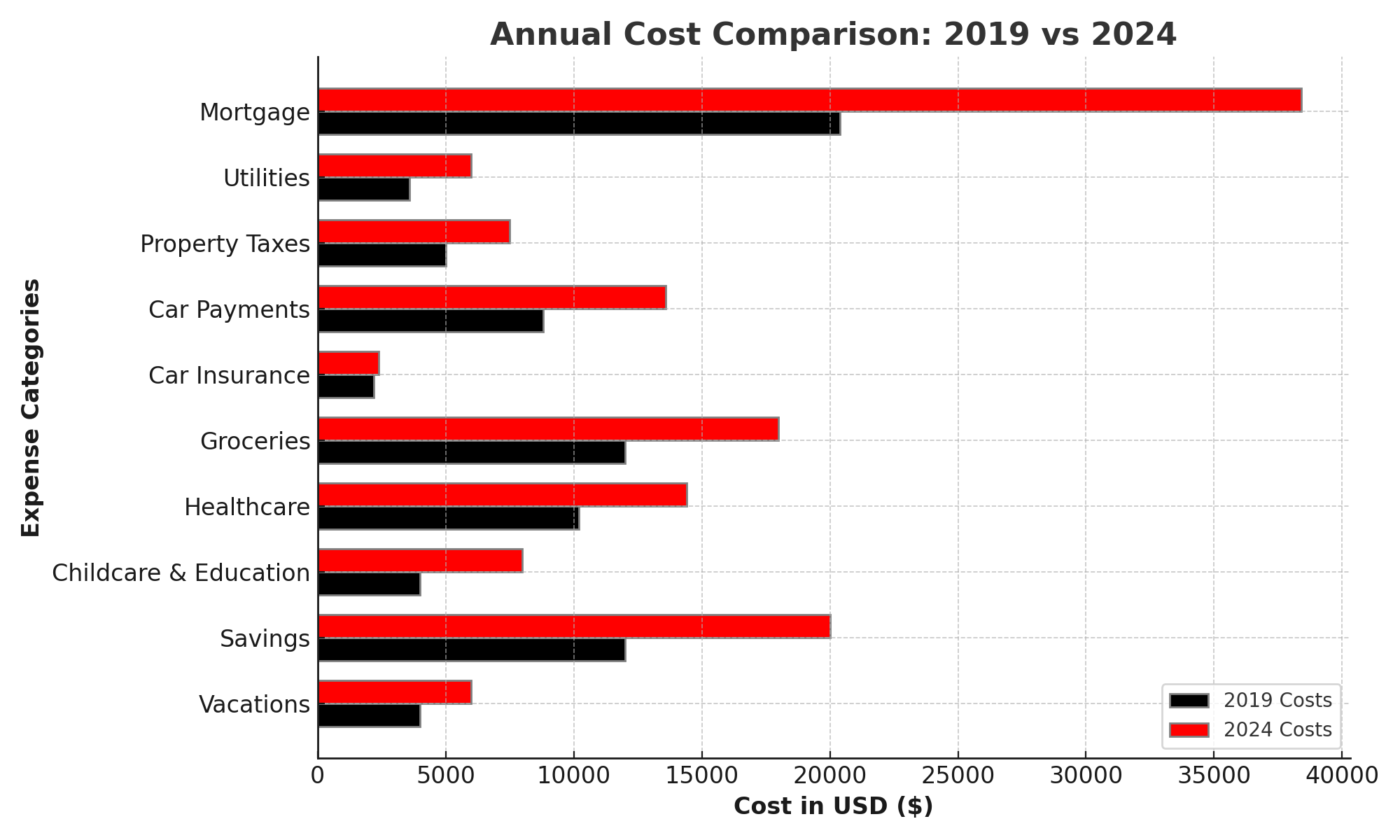

This report provides a comprehensive comparison of the real inflation rates based on specific living costs in Austin, Texas, from 2019 to 2024. We analyze major expenses such as housing, cars, utilities, and savings to show how much costs have risen in five years. The Consumer Price Index (CPI) suggests a rise of about 18-20%, but this analysis reveals real inflation, as felt by the average household, is closer to 44.1%.

Detailed Breakdown of Costs and Inflation:

We will now look at each major category of expenses, comparing the estimated costs in 2019 and 2024, and calculate the percentage increase for each category. These categories include mortgage payments, car expenses, groceries, healthcare, and other necessary costs for a family of five living in Austin. The data assumes that the family has a stay-at-home parent and two used vehicles, and we include the cost of saving for emergencies, retirement, and children’s education.

Math and Calculation Details

1. Mortgage Costs:

In 2019, the median home price in Austin was around $350,000. With a 20% down payment and a 30-year mortgage at 4.0% interest, the monthly payments were around $1,700-$1,800, leading to an annual cost of approximately $20,400-$21,600.

In 2024, the median home price increased to about $500,000. With the same down payment but higher interest rates (around 7.5%), monthly payments increased to $3,000-$3,200, resulting in an annual cost of $36,000-$38,400.

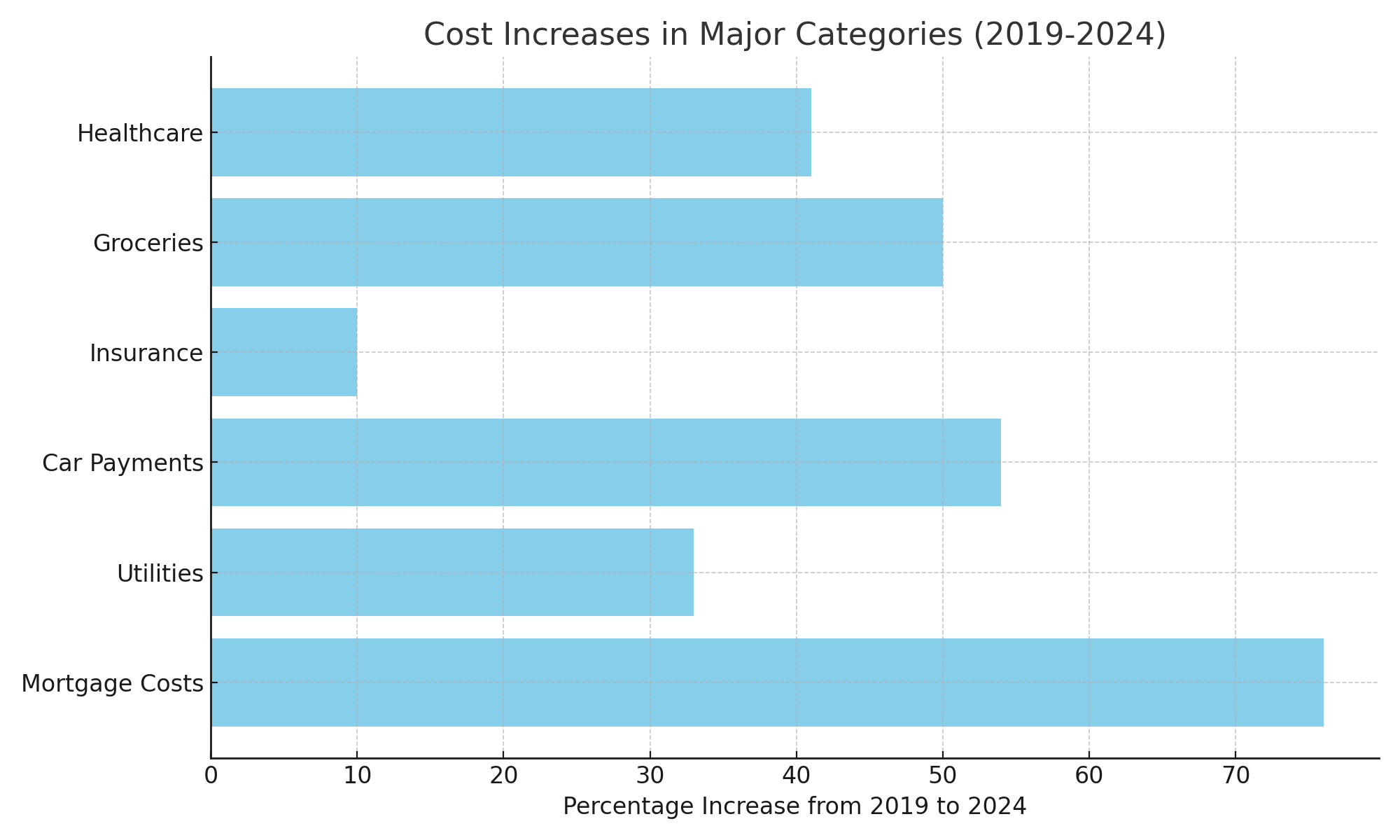

**Percentage Increase**: Approximately 76% increase in mortgage costs.

2. Utilities:

In 2019, average utility costs for a family of five were around $300 per month, totaling about $3,600 annually.

By 2024, these costs rose to $400-$500 per month, leading to an annual cost of $4,800-$6,000.

**Percentage Increase**: 33% to 66% increase, depending on usage.

3. Car Payments and Insurance:

In 2019, a used car cost around $20,000-$25,000, with monthly payments around $370-$460 for each vehicle. Total annual car payments were about $8,800 for two cars. Insurance averaged $1,100 per year per car.

In 2024, used car prices rose to about $30,000 per car. Monthly payments increased to around $566 per car, leading to $13,600 per year for two vehicles. Insurance increased slightly to $1,200 per car annually.

**Percentage Increase**: Car payments increased by 54%, and insurance by about 9%.

4. Groceries:

In 2019, groceries for a family of five cost about $1,000 per month, or $12,000 per year.

By 2024, this had risen to $1,400-$1,500 per month, resulting in an annual cost of $16,800-$18,000.

**Percentage Increase**: 40% to 50% increase in grocery costs.

5. Healthcare:

In 2019, the average health insurance premium for a family was around $850 per month, totaling $10,200 annually.

By 2024, premiums had increased to about $1,200 per month, leading to $14,400 per year in healthcare costs.

**Percentage Increase**: 41% increase in healthcare costs.

Total Bottom Line Inflation: 2019 vs. 2024

Taking into account all the categories of expenses, the total cost of living for a family of five in Austin increased from approximately $96,150-$100,950 in 2019 to $137,800-$146,200 in 2024. This represents a total increase of 44.1% over five years.

This level of real inflation highlights the growing difficulty for families to maintain the same standard of living with a $100K income in 2024 compared to 2019.

Impact of Real Inflation on $100,000 Salary

If you earned $100,000 in 2019, due to 44.1% inflation, that income today only has the buying power of about $69,400. The significant rise in housing, groceries, healthcare, and other costs has eroded purchasing power. Below, we analyze specific categories, showing how much expenses have increased from 2019 to 2024, with visual aids to emphasize the differences.

Based on the comprehensive data and analysis we've covered, it's reasonable to conclude that the middle class is facing significant economic pressure, if not outright erosion, for several reasons:

1. Wages Stagnating vs. Costs Soaring

Wage Growth: Wages in the U.S. have not increased in proportion to the rise in living costs over the past five years. Median wage growth has been slow and uneven, with many middle-class workers seeing stagnant incomes.

Real Inflation: As shown, real inflation for key expenses like housing, healthcare, and groceries has increased by 44.1% since 2019. When wage growth doesn’t keep pace with inflation, the middle class struggles to maintain its standard of living.

Reduced Buying Power: Earning $100K in 2019 is now like earning $69,400 today. This erosion in purchasing power translates to greater difficulty in affording necessities, let alone saving for retirement, vacations, or emergencies.

2. Housing Affordability Crisis

Housing costs, one of the most significant expenses for families, have skyrocketed in major cities like Austin, making it harder for middle-class families to afford homes without stretching their finances. Mortgage rates have increased as well, compounding this issue.

This is a major factor in the shrinking wealth-building opportunities for the middle class, which traditionally relied on homeownership to accumulate equity.

3. Rising Cost of Essentials

Essentials like healthcare, education, utilities, and groceries have become disproportionately expensive compared to wage growth. This puts middle-class families in a precarious position, where more of their income is funneled into basic needs, leaving little room for saving or investing.

4. Impact on Savings and Retirement

As savings and retirement funds become harder to maintain, especially with higher costs, many middle-class families are unable to meet recommended savings targets. This erodes long-term financial security, setting the stage for a less stable retirement.

5. Shrinking Disposable Income

With a larger portion of income going to necessary expenses, middle-class families have less disposable income for discretionary spending, which historically fuels economic growth and quality of life improvements.

The ability to afford vacations, entertainment, and even emergency expenses is being reduced, making the middle class more vulnerable to financial shocks.

Conclusion of the analysis on inflation

This analysis demonstrates how the cost of living for a family in Austin has increased by approximately 44.1% over five years. Households earning $100,000 in 2019 have much less purchasing power today, struggling to cover increased mortgage payments, utilities, groceries, and healthcare costs. Adjusting for inflation, $100,000 in 2019 now feels like just $69,400 in 2024, making it harder for families to maintain the same standard of living.

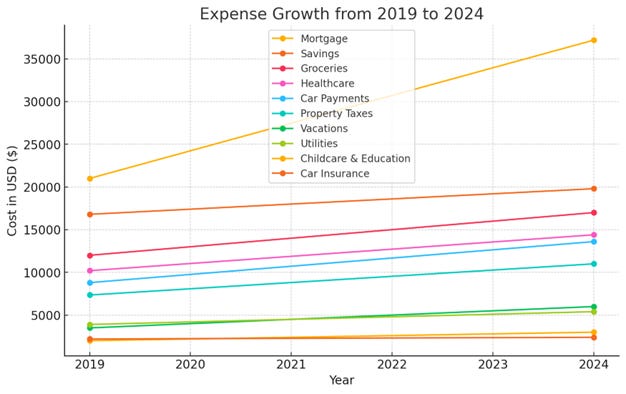

Additional Visuals and Data Analysis

Cost Increases in Major Categories (2019-2024):

Updated Focus on 2021-2024 Economic Hardship

This analysis focuses on the worsening economic conditions from the beginning of 2021 through 2024, emphasizing the impact of inflation, wage stagnation, and the surge in layoffs during July and August of 2024. While the Consumer Price Index suggests modest inflation, this analysis reveals how middle-class families have been hit with significant price increases across essential categories, further compounded by the massive layoffs and economic instability.

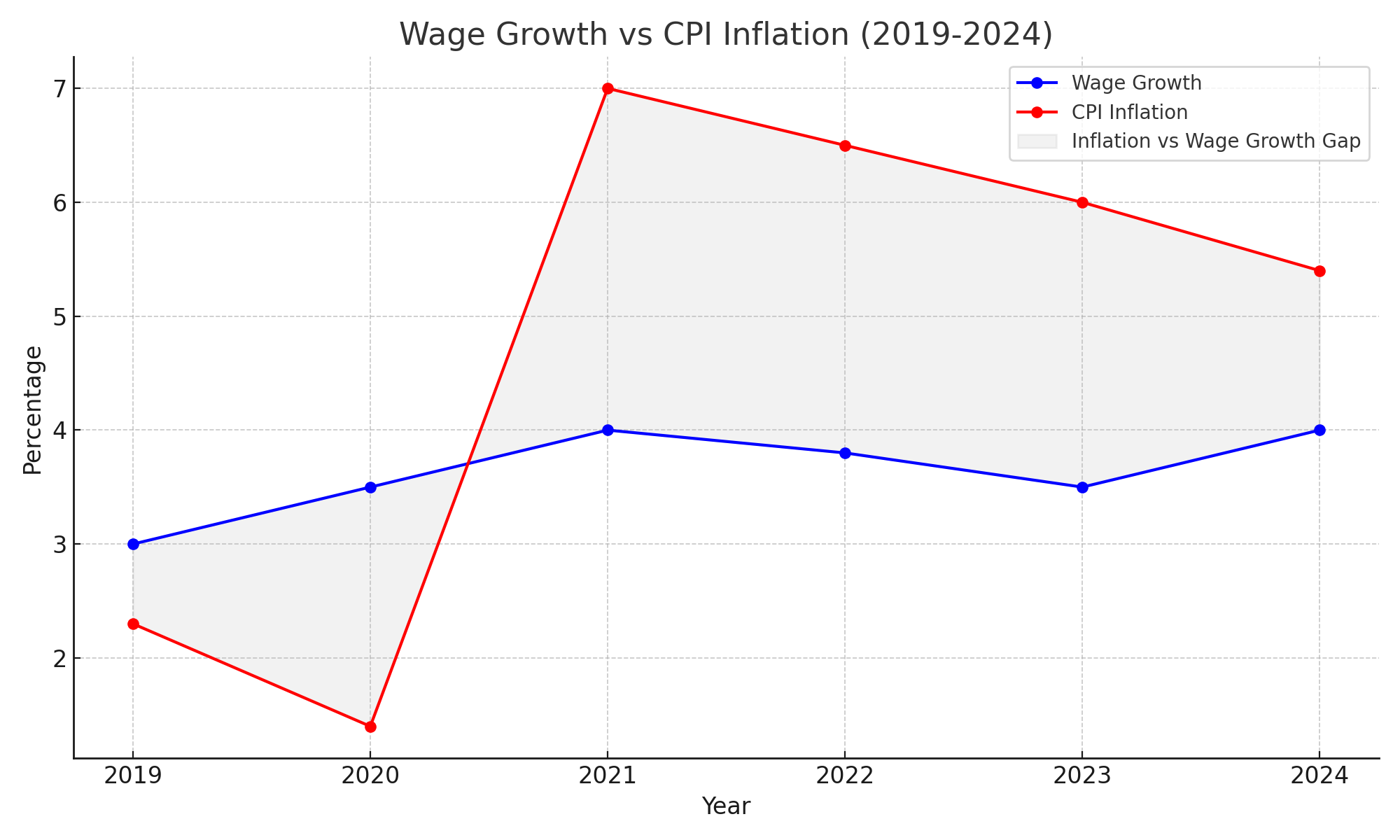

Wage Growth vs CPI Inflation

The following visualization compares wage growth with the Consumer Price Index (CPI) from 2019 to 2024. This graph shows how consumer inflation, as measured by the CPI, continues to outpace wage growth over the past five years. While wage growth appears modest, real inflation has severely impacted purchasing power, demonstrating the growing economic strain on middle-class families.

Impact of Ukraine Spending and Money Circulation

Since 2022, the U.S. has committed a staggering $175 billion in aid to Ukraine. While some of this money was spent on domestic defense production, only $106 billion went directly to aid Ukraine. This allocation has taken priority over domestic concerns, leaving middle-class families in the U.S. grappling with rising inflation, stagnant wages, and layoffs. The foreign aid spending could have been redirected to combat inflation domestically, easing economic pressure on Americans.

Meanwhile, the U.S. money supply has surged since the end of 2019, growing from $15 trillion to over $21 trillion by 2024. This 40% increase has contributed to inflation, as a larger money supply decreases the dollar's value, driving up the prices of goods and services. The combination of massive foreign spending and a growing money supply has left American families struggling to cope with the rising costs of essential goods.

The Real Impact of the Inflation Reduction Act

While the Inflation Reduction Act (IRA) was sold as a solution to inflation, much of its $369 billion in spending was allocated toward green energy subsidies and infrastructure, particularly for electric vehicles (EVs). While this has helped create jobs, particularly in U.S.-based industries like Tesla, it has done little to address the immediate inflationary pressures faced by middle-class families.

Instead of focusing on long-term environmental projects, the funds could have been used to provide short-term relief to families struggling with rising housing, healthcare, and grocery costs. The IRA's investments, though beneficial for the future, do not help the current crisis and have left many middle-class families feeling the brunt of inflation.

Conclusion: 2021-2024 - The Worst Economic Period in Modern History!

The period from 2021 to 2024 has seen some of the most damaging effects on the middle class in history, especially in growing cities like Austin. Despite the government's efforts to downplay inflationary pressures, the real cost of living has skyrocketed. The combination of stagnant wage growth, massive layoffs, and sharp increases in housing, utilities, groceries, and healthcare costs have put immense strain on middle-class families.

The surge in layoffs during July and August 2024 further highlights the severe instability that defines this period. This analysis shows that, rather than improving, economic conditions have worsened dramatically over the past three years, leaving many families struggling to just to make ends meet that were thriving economically in 2019.